On July 14, 2013, we published a fact check of a claim from Consumer Reports’ website about the supposed savings for medical insurance consumers as a result of the health care reform bill, the Affordable Care Act. The fact check omitted a significant aspect of the story and reached some false conclusions about writer Nancy Metcalf’s story, including “Metcalf misrepresents the Kaiser study’s content.”

While reviewing Glenn Kessler’s fact check of a similar claim, we realized we had failed to keep in focus the source Metcalf used for her story. Metcalf relied on information from Centers for Medicare & Medicaid Services, under the Department of Health and Human Services and DHS Secretary Kathleen Sebelius, and the fact check should have included a reference to that material in the “References” section. Metcalf did not refer to the findings of the Kaiser study and therefore did not misrepresent its findings. We apologize to Metcalf and our readers for the error, and have revised and republished the fact check to fix the errors and clarify our criticism of the data underlying Metcalf’s claim.

Below, we have reproduced the text of the original fact check as it appeared on July 24, 2013, when we announced our intent to revise the fact check.

Editor’s note July 24, 2013: We’ve detected some problems with this fact check, stemming from a failure to sustain focus on the HHS report that served as the source for the Consumer Reports story. Look for a new version of this story to take the place of this one over the next few days, with a full explanation (and an archived version of the present state of the post) in our Corrections section.

“[The Affordable Care Act] has already saved consumers billions.”

“[The Affordable Care Act] has already saved consumers billions.”

—Nancy Metcalf, Consumer Reports, June 21, 2013

Overview

The Consumer Reports claim ignores all the ways the ACA costs consumers money as well as the effects of other cost-saving features in the bill.

The Facts

On June 21, 2013, Consumer Reports published an online article by Nancy Metcalf touting the benefits of Obamacare, specifically savings on premiums.

Metcalf:

From time to time I hear from readers who are convinced the Affordable Care Act will ruin us all financially. Not happening so far. Instead, it has already saved consumers billions.

Exhibit A: In 2012, the law directly saved consumers $3.4 billion on their insurance premiums, and will require insurance companies to rebate another $500 million in premium overcharges this summer. This is all thanks to a part of the law that requires insurance companies to spend at least 80 cents of every dollar of premium they collect on health care for their customers. If they spend less than that, they have to refund the difference.

Obamacare, also known as the Affordable Care Act, does include mandated minimum levels for insurance companies’ medical loss ratios. The MLR is the percentage of premium income used on health care benefits or “activities that improve the quality of care.”

The ACA sets the minimum MLR at 80 percent for the individual market and at 85 percent for the group market. The law sets the figure higher for the group market because the larger number of enrollees allows for lower overhead costs as a percentage of premiums. If companies do not meet the ACA standard, they must refund to customers any excess premiums charged that push the MLR below the minimum allowed.

Earlier in June, the Kaiser Family Foundation published a study estimating premium savings stemming from the ACA’s limits on MLRs. The study said consumers could save money via the MLR policy via rebates or by lower premiums that result from companies trying to avoid giving rebates.

“[I]t is hard to know with certainty what premiums would have been if the MLR rules were not in place: we cannot know for sure how insurers would have priced their products or what rates regulators would have allowed (to the extent that they reviewed rates prior to the ACA). It is also difficult to separate out the direct effects of the MLR provision from other aspects of the health reform law, particularly rate review, which works to moderate unreasonable premium increases and thus increase loss ratios. There are also data limitations. For example, prior to new reporting requirements put in place to enforce the MLR provision, there were not good data sources that break out premiums and claims on a consistent basis for major medical coverage by all types of carriers. In the initial years this data became available (2010 and 2011), there were some issues with the quality of the data, particularly regarding expenses for quality improvement and other new categories of administrative expenses that are reported on the exhibit.

So from a research standpoint, this study faces the challenges of finding a baseline for comparison and isolating the effect of the ACA’s limits on MLRs.

Analyzing the Rhetoric

We’ll examine the Kaiser Family Foundation study before analyzing the rhetoric about consumer savings from Consumer Reports.

The Kaiser study identifies a number of limitations with its research approach. The list of limitations could have been longer. Commentators such as Sally Pipes and Avik Roy have pointed out ways in which the ACA’s minimum limits on MLRs could increase premiums. The Kaiser study ignores such possibilities. Also, for the period examined in the study, health care costs have increased more slowly than normal. The Kaiser Family Foundation published a study earlier this year identifying the slow economy as the primary cause of the slowdown. Unexpectedly low health care spending implies a tendency to set premium prices abnormally high in relation to medical costs. After all, insurance companies set rates before paying claims on policies in a given year.

Though Kaiser’s study of savings from mandating MLR levels acknowledges that insurance companies started to adjust to the requirements from 2011 to 2012, it ignores perhaps the most significant adjustment: taking into account the national slowdown in health care spending. That oversight figures in particularly when Kaiser estimates customer savings, basing its estimates simply on what premiums might have cost if MLRs failed to improve from 2011 to 2012:

Premium savings for each year represent estimates of what consumers would have spent if the ratio of claims to premiums had stayed at 2010 levels. For example, individual market premium savings in 2011 were calculated by subtracting the inverse of the weighted average individual market MLR in 2011 from the inverse of the weighted average individual market MLR in 2010, then multiplying the result by the total individual market claims in 2011.

The authors of the Kaiser study do not hide its weaknesses. But politicians and journalists reporting about the study have tended to present the findings without the caveats. Given what it overlooks, questioning the value of the study makes good sense.

Consumer Reports does not question the value of the study at all. On the contrary, Metcalf’s article ignores the Kaiser study’s own caveats and attributes the whole of the estimated savings to the ACA’s medical loss ratio targets (bold emphasis added):

This is all thanks to a part of the law that requires insurance companies to spend at least 80 cents of every dollar of premium they collect on health care for their customers.

It’s bad enough that Metcalf failed to inform readers about the full contents of the report as well as factors that went totally unmentioned in the report. But Metcalf also failed to disclose to her readers a potential personal bias. Metcalf donated no less than $1,750 to the Obama campaign for the 2012 election cycle, according to FEC records.

More on the ACA’s medical loss ratio provisions

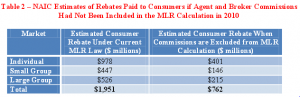

Insurance brokers have fought for an amendment to the ACA that would exempt insurance companies from counting their sales commissions as overhead when calculating MLRs and premium rebates.

Insurance brokers have fought for an amendment to the ACA that would exempt insurance companies from counting their sales commissions as overhead when calculating MLRs and premium rebates.

Democrats have fought that measure, saying it would greatly reduce the savings provided to consumers:

H.R. 1206 would reduce the $1 billion consumer premium rebates by at least $360 million, increasing premiums for 3.8 million people in Delaware, Florida, Indiana, Kansas, Louisiana, Michigan, North Dakota, Oklahoma, Texas, and Wisconsin.

The Congressional Budget Office estimated the effects of H.R. 1206 and agreed that much of the current improvement of MLRs comes at the expense of insurance agents and brokers (bold emphasis added):

For 2011 and 2012, CBO estimated the magnitude of the reduction in premiums resulting from the MLR policy. That estimate draws on insurance industry data and is based on two factors: actual rebates in 2012, and evidence that insurance carriers reduced administrative costs (in large part by reducing agent and broker compensation).

The CBO went on to assess that savings from the policy would tend to tail off (bold emphasis added):

Beyond 2012, in CBO’s judgment, the MLR policy under current law will continue to have the effect of reducing premiums relative to those in the absence of that policy. Over time, however, CBO expects that the reduction in premiums will be attenuated. Starting in 2014, a three-year moving average, rather than annual data, will be used to calculate the MLR, making the MLR targets easier to achieve. In addition, CBO expects that there is an increasing probability that insurers will make changes – such as increasing spending on medical benefits or quality improvement activities – that will push premiums upward.

As the critics have noted, the MLR provision creates a disincentive for insurers to control spending on medical treatment and “quality improvement activities.” For example, it will make little sense for an insurance company to fight fraud if its MLR falls close to the limit set by the health care law. The potentially misspent money helps raise the MLR, and spending to recoup misspent money lowers the MLR. The cost of administrating compliance with the MLR rules also lowers the MLR.

The Kaiser study makes its biggest mistake in calculating consumer saving from the health care law’s MLR provisions without regard for effects from other parts of the law. The study ends up giving an optimistic figure from gross savings from the MLR policy in isolation instead of giving a picture of the net costs to consumers stemming from the health care reform law. Consumer Reports magnifies the Kaiser Family Foundation’s error by erasing the caveats and reporting the optimistic conclusion as a simple fact.

It seems safe to say that the ACA has cost insurance agents millions with its medical loss ratio limits. If insurance agents do not offer a valuable service then consumers have derived a benefit from saving that expense.

Summary

“[The Affordable Care Act] has already saved consumers billions.”

![]()

Given the Kaiser study’s multiple methodological problems, one can only regard the claim as true by ignoring increased costs and assuming the study’s estimate approaches the truth by accident. The claim leaves out caveats in the original study and leaves out all mention of factors that increase insurance premiums, resulting in a fallacy of one-sidedness. Based as it is on the Kaiser study, the claim rests on a form of the Texas Sharpshooter fallacy, picking out stats that supposedly show a reduction in premiums attributable to the MLR guidelines. But the data may have a different meaning.

“This is all thanks to a part of the law that requires insurance companies to spend at least 80 cents of every dollar of premium they collect on health care for their customers.”

![]()

Metcalf misrepresents the Kaiser study’s content. The study does not claim that all the estimated savings occurred because of MLR guidelines. On the contrary, the study warns of the difficulty in ruling out other factors. Metcalf’s description of the MLR guidelines also contains ambiguity and inaccuracy, for group plans need to spend no less than 85 cents on the dollar and spending on efficiencies, not just health care, can contribute toward meeting the minimum spending goal.

References

Metcalf, Nancy. “Could It Be That Obamacare Is Actually Saving Money?” Consumer Reports. Consumer Reports, 21 June 2013. Web. 10 July 2013.

“Glossary: Medical Loss Ratio (MLR).” HealthCare.gov. U.S. Centers for Medicare & Medicaid Services, n.d. Web. 10 July 2013.

Cox, Cynthia, Gary Claxton, and Larry Levitt. “Beyond Rebates: How Much Are Consumers Saving from the ACA’s Medical Loss Ratio Provision?” The Henry J. Kaiser Family Foundation. Kaiser Family Foundation, 6 June 2013. Web. 10 July 2013.

Cox, Cynthia, Gary Claxton, and Larry Levitt. “Beyond Rebates: How Much Are Consumers Saving from the ACA’s Medical Loss Ratio Provision?: Methodology.” The Henry J. Kaiser Family Foundation. Kaiser Family Foundation, 6 June 2013. Web. 10 July 2013.

Pipes, Sally. “MLR Is Only the Beginning of the End of Private Health Insurance in America.” MedCity News. MedCity News, 25 Mar. 2012. Web. 13 July 2013.

Roy, Avik. “Obamacare’s MLR ‘Bomb’ Will Create Private Insurance Monopolies and Drive Premiums Skyward. Hallelujah!” Forbes. Forbes Magazine, 06 Dec. 2011. Web. 13 July 2013.

McCue, Michael J., and Mark A. Hall. “Insurers’ Responses to Regulation of Medical Loss Ratios.” The Commonwealth Fund. The Commonwealth Fund, 5 Dec. 2012. Web. 10 July 2013.

McCue, Michael J., and Mark A. Hall. “Insurers’ Responses to Regulation of Medical Loss Ratios.” The Commonwealth Fund. The Commonwealth Fund, 5 Dec. 2012. Web. 10 July 2013.

“Private Health Insurance: Early Experiences Implementing New Medical Loss Ratio Requirements.” U.S. GAO. U.S. Government Accountability Office, 29 July 2011. Web. 10 July 2013.

“Private Health Insurance: Early Experiences Implementing New Medical Loss Ratio Requirements.” U.S. GAO. U.S. Government Accountability Office, 29 July 2011. Web. 10 July 2013.

“Milliman Study Highlights the Impact of Medical Loss Ratio Rules on HSAs.” American Bankers Association. American Bankers Association, 13 Feb. 2012. Web. 10 July 2013.

“Health Reform’s Medical Loss Ratio Rebates — A Good Value for Consumers?” NAHU.org. National Association of Health Underwriters, n.d. Web. 10 July 2013.

Postal, Arthur D., and Allison Bell. “CBO: Agent Comp Bill Could Add $1.1 Billion to Deficits.” LifeHealthPro. LifeHealthPro, 8 Nov. 2012. Web. 10 July 2013.

“H.R. 1206: Access to Professional Health Insurance Advisors Act of 2011.” CBO.gov. Congressional Budget Office, 7 Nov. 2012. Web. 10 July 2013.

“New Survey Shows Devastating Effects of Medical Loss Ratio on Health Insurance Agents, Consumers.” NAIFA. National Association of Insurance and Financial Advisors, 29 Apr. 2011. Web. 10 July 2013.

“Health Agents and Consumers Hurt by MLR.” NAIFA. National Association of Insurance and Financial Advisors, Apr. 2011. Web. 10 July 2013.

Harris, Spencer. “Medical Loss Ratios.” Texas Public Policy Foundation. Texas Public Policy Foundation, Jan. 2012. Web. 10 July 2013.

Harris, Spencer. “Medical Loss Ratios.” Texas Public Policy Foundation. Texas Public Policy Foundation, Jan. 2012. Web. 10 July 2013.

“Assessing the Effects of the Economy on the Recent Slowdown in Health Spending.” The Henry J. Kaiser Family Foundation. Kaiser Family Foundation, 22 Apr. 2013. Web. 10 July 2013.

“Consumer Health Insurance Savings Under the Medical Loss Ratio Law.” U.S. Senate Committee on Commerce, Science, & Transportation. United States Senate, 24 May 2011. Web. 11 July 2013.

“Consumer Health Insurance Savings Under the Medical Loss Ratio Law.” U.S. Senate Committee on Commerce, Science, & Transportation. United States Senate, 24 May 2011. Web. 11 July 2013.

Heal, Loren. “Funny Math: The Government Pretends They Save You Money.” FreedomWorks.org. FreedomWorks, 26 June 2013. Web. 11 July 2013.

Meulemans, Michael. “Health Insurance Rebate Analysis.” About.com Insurance. About.com, n.d. Web. 11 July 2013.

“The Check Is in The Mail…Well, Maybe.” NAHU Washington Update. National Association of Health Underwriters, 30 Apr. 2012. Web. 11 July 2013.

<background=white>”Medical Loss Ratio Rebates Paid in 2013 – Frequently Asked Questions.” CareFirst.com. CareFirst BlueCross BlueShield, n.d. Web. 11 July 2013.

Laszewski, Bob. “Flawed Analysis––Medical Loss Ratio Rules Led to $1.9 Billion in Lower Premiums.” Health Care Policy and Marketplace Review. Health Policy and Strategy Associates, LLC, 7 June 2013. Web. 11 July 2013.

Book, Robert. “How the Medical Loss Ratio Requirement Could Increase Health Insurance Premiums And Insurer Profits at Taxpayer Expense.” American Action Forum. American Action Forum, Apr. 2013. Web. 11 July 2013.

Jacobs, Chris. “Ezra Klein Can’t Save Obamacare’s Broken Premium Promise.” The Foundry Conservative Policy News Blog. The Heritage Foundation, 13 June 2013. Web. 11 July 2013.

Kirchhoff, Suzanne M., and Janemarie Mulvey. “Medical Loss Ratio Requirements Under the Patient Protection and Affordable Care Act (ACA): Issues for Congress.” Congressional Research Service/FAS.org. Federation of American Scientists, 18 Sept. 2012. Web. 11 July 2013.

Kliff, Sarah. “How Will Obamacare Hit Premiums? Let’s Break down the Numbers.” The Washington Post Wonkblog. The Washington Post Company, 29 Mar. 2013. Web. 11 July 2013.

Corlette, Sabrina. “The Medical Loss Ratio Rule – Report Highlights Savings for Consumers.” CCF. Georgetown University Health Policy Institute, 9 Dec. 2012. Web. 11 July 2013.

Brino, Anthony. “CMS Cites MLR in Premium Cost Control.” Healthcare Payer News. MedTech Media, 20 June 2013. Web. 11 July 2013.

Caplan, Jesse M. “Musings on the MLR.” PPACA Impact and Opportunities. Epstein Becker & Green, P.C., 4 Oct. 2012. Web. 11 July 2013.

Britt, Russ. “Whoa, Insurers Say — Spend Rules Unlikely Cause of Premium Savings.” Health Exchange. MarketWatch, Inc., 20 June 2013. Web. 11 July 2013.

Kliff, Sarah. “Obamacare Saved Consumers $1.5 Billion — and That’s Bad News for Insurers.” The Washington Post Wonkblog. The Washington Post Company, 5 Sept. 2012. Web. 11 July 2013.

Suderman, Peter. “ObamaCare’s Health Insurance Rebates May Make Insurance More Expensive.” Reason.com. Reason Foundation, 21 Sept. 2012. Web. 11 July 2013.

Kestenbaum, David. “Insurance Companies Send Out Rebate Checks; Economists Get Nervous.” NPR. NPR, 20 Sept. 2012. Web. 11 July 2013.

Lambrew, Jeanne. “Good News: Americans Saved Billions Thanks to the Affordable Care Act – And Medical Loss Rebates Are On the Way.” The White House Blog. The White House, 6 June 2013. Web. 11 July 2013.

Suderman, Peter. “Is ObamaCare Causing Premiums to Rise?” Is ObamaCare Causing Premiums to Rise? RealClearPolitics, 8 Jan. 2013. Web. 11 July 2013.

Cauchi, Richard, and Steven Landess. “Medical Loss Ratios for Health Insurance.” NCSL.org. National Conference of State Legislatures, 20 June 2013. Web. 11 July 2013.

Mahon, Mary, and Bethanne Fox. “New Report: Insurers on Average Spent Less Than 1 Percent of Premium Dollars on Health Care Quality Improvement Activities in 2011.” The Commonwealth Fund. The Commonwealth Fund, 22 Mar. 2013. Web. 11 July 2013.

“Assessing the Implications of the Medical Loss Ratio (MLR) Requirement.” HCFO. The Changes in Health Care Financing & Organization Initiative, Sept. 2012. Web. 11 July 2013.

“New Study Shows Costs of MLR Regulation Higher Than Originally Thought.” AHIP Coverage. AHIP Coverage, 6 June 2011. Web. 11 July 2013.

“The Federal Medical Loss Ratio (MLR) Calculations – Background and Initial Costs of Compliance.” AHIP Center for Policy and Research. AHIP Coverage, June 2011. Web. 11 July 2013.

“Medical Loss Ratio (MLR).” Healthcare Choice Coalition. Healthcare Choice Coalition, n.d. Web. 11 July 2013.

Ramthun, Roy. “MLR Regulation Creates Challenges for Future of Affordable Coverage.” Healthcare Choice Coalition. HSA Consulting Services, LLC, 27 Dec. 2011. Web. 11 July 2013.

Anderson, Chris. “MLR Regs Saved Consumers $2.1B in 2012.” Healthcare Payer News. MedTech Media, 10 June 2013. Web. 12 July 2013.

“Penn LDI : Analysis.” Leonard Davis Institute of Health Economics. Leonard Davis Institute, n.d. Web. 12 July 2013.

Brittenham, Marissa. “Impact of Medical Loss Ratio “Expenditures to Improve Health Quality” Definition on Wellness Programs.” Leonard Davis Institute of Health Economics. Leonard Davis Institute, n.d. Web. 12 July 2013.

Reichel, Randi F., Esq. “Medical Loss Ratios: 2011 and Beyond.” MHPA.org. Medicaid Health Plans of America, 3 Feb. 2011. Web. 12 July 2013.

Additional Note

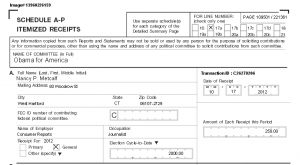

It’s also appropriate to provide some direct documentation of Nancy P. Metcalf’s political preference, for it relates to her failure to disclose to readers of Consumer Reports a potential bias. The FEC makes available images of the receipts from political giving above certain thresholds. Find many more such records of Metcalf’s political giving through FEC.gov.

Related Posts

Correction to correction request description

Correction to correction request description- Correction: Substituted duplicate IFCN complaint for a different complaint

Misspelled ‘Demings’

Misspelled ‘Demings’- Correction to ZFC critique of PolitiFact's 'Medicare For All" explainer

- Corrections to our critique of Aaron Huertas and the Poynter Institute

- Wrong date on Jefferson’s letter to Col. Humphries